Bplus新加坡

Bplus新加坡

权威解读新加坡MAS最新版《数字代币发行指南》及11个案例分析

2017年8月1日,新加坡金管局(MAS)正式发表关于1CO监管的声明性文件,表示将对涉及到 “新加坡证券与期货法(SFA)” 的1CO活动进行监管,这是MAS第一次正面出台1CO监管文件。www.lianhuo18.com

三个月多后的11月14日,MAS发布了《数字代币发行指南》(A Guide to Digital Token Offerings,下称《指南》),该《指南》被视为MAS对1CO监管的澄清性文件,MAS也在其中对监管过程和范围给出了更清晰的说明。

上周五(11月30日),MAS又在去年《数字代币发行指南》的基础上,针对市场中出现的新情况和新模式,如不断涌现的代币交易平台和STO,推出了更新版的《指南》。

“新版《指南》增设的重点与解析”

相比于去年的版本,今年最新的版本主要新增和强调了以下几个方面的内容:

一、对反洗钱和打击恐怖主义融资(AML/CFT)的监管力度加强,MAS这次不仅专门指出了AML/CFT的适用范围,还对AML/CFT的具体要求做出了说明。

在AML/CFT的适用范围上,从事MAS在2.8-2.11段所描述的一项或多项活动的中间人,且满足下列要求,就适用于AML/CFT的监管:

1.Holder of a capital markets services licence under the SFA(根据SFA持有资本市场服务牌照);

2.Fund management company registered under paragraph 5(1)(i) of the Second Schedule to the Securities and Futures (Licensing and Conduct of Business) Regulations (Rg. 10) (“SF(LCB)R”)(基于证券及期货规例(Rg. 10) (“SF(LCB)R”)附表2中的5(1)(i)内容注册的基金管理公司);

3.Person exempted under paragraph(s) 3(1)(d), 3A(1)(d) and/or 7(1)(b) of the Second Schedule to the SF(LCB)R from the requirement to hold a capital markets services licence(根据根据SF(LCB)R附表2第3(1)(d),3A(1)(d) 或者 7(1)(b)段获豁免持有资本市场服务许可牌照的人);

4.Licensed financial adviser under the FAA(《金融顾问法》)(FAA下的持牌财务顾问);

5.Registered insurance broker which is exempt under section 23(1)(c) of the FAA from holding a financial adviser’s licence to act as a financial adviser in Singapore in respect of any financial advisory service(根据FAA第23(1)(c)条获豁免的,持有财务顾问牌照,以就任何财务顾问服务在新加坡担任财务顾问的注册保险经纪人);

6.Person exempt under section 23(1)(f) of the FAA read with regulation 27(1)(d) of the Financial Advisers Regulations (Rg. 2) from holding afinancial adviser’s licence to act as a financial adviser in Singapore in respect of any financial advisory service(基于FAA section 23(1)(f)条款,参照“财务顾问条例”(第2条)第27(1)(d)条的规定,获得金融顾问牌照豁免,但仍然从事金融顾问业务的个人);

对AML/CFT的具体要求,MAS的更新版指南规定如下:

1. Take appropriate steps to identify, assess and understand their money laundering and terrorism financing (ML/TF) risks(采取适当步骤,以识别、评估和了解他们的洗钱和恐怖主义融资(ML / TF)风险);

2. develop and implement policies, procedures and controls – including those in relation to the conduct of customer due diligence and transaction monitoring, screening, reporting suspicious transactions and record keeping – in accordance with the relevant MAS Notices, to enable them to effectively manage and mitigate the risks that have been identified(制定和实施包括与客户尽职调查和交易监控,筛选,报告可疑交易和记录保存相关的政策,程序和控制 - 根据相关的MAS通知,使其能够有效管理并降低已发现的风险);

3. perform enhanced measures where higher ML/TF risks are identified, to effectively manage and mitigate those higher risks(在确定更高洗钱及恐怖主义风险的情况下执行增强措施,以有效管理和降低这些高风险);

4. monitor the implementation of those policies, procedures and controls, and enhance them if necessary(监督这些政策,程序和控制的实施,并在必要时予以增强);

二、对涉及到证券的代币产品的增加。除了去年提到的股票、债券和集合投资计划(“CIS”)单位基金外,今年还增加了两个类型:

1. A unit in a business trust7, where it confers or represents ownership interest in the trust property of a business trust(单位商业信托,代表了对该商业信托基金的所有权);

2. A securities-based derivatives contract8, which includes any derivatives contract of which, the underlying thing is a share, debenture or unit in a business trust(基于证券的衍生品合约,包括任何基于股票、债券或单位商业信托的衍生品合约);

三、依据即将推出的《支付服务法案》(Payment Services Bill, "PSB"),MAS对从事支付型代币交易相关业务的公司的监管进一步清晰化,这主要体现在需获得相应牌照,以及在AML/CFT方面受PSB的监管。

MAS has introduced the Payment Services Bill ("PSB") in Parliament on 19 November 2018. A person carrying on a business of providing any service of dealing in digital payment tokens or any service of facilitating the exchange of digital payment tokens must be licensed and will be regulated under the PSB for AML/CFT purposes only and will be required to put in place policies, procedures and controls to address its ML/TF risks.

(MAS于2018年11月19日在议会提出了PSB。从事提供任何数字支付代币交易服务或任何促进数字支付代币交换服务的人必须获得牌照,并将仅在洗钱和恐怖主义方面受PSB管制,而且需要制定政策,程序和控制措施来解决其洗钱/恐怖主义风险。)

“MAS代币发行监管案例与解读”

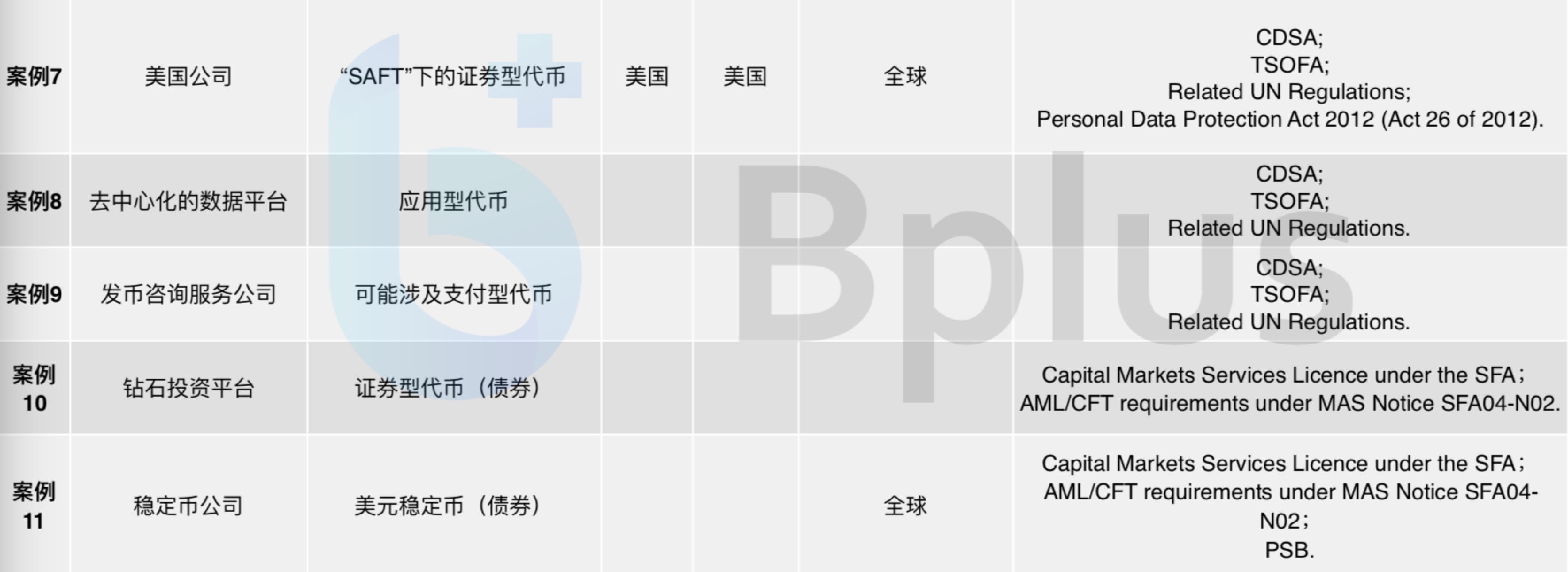

在最新版指南中,MAS也在之前的基础上增加了5个案例,即这次共提供了11个案例作为参考,以让发行不同性质的代币或从事相关业务的公司,对可能涉及到的监管法规有一个更加清晰的认识。

我们也独家解析了两个关于STO股权融资和支付型代币交易平台的典型案例,并对11个案例中所涉及到活动和相关监管法规进行了归纳总结。

案例2:Company B is in the business of developing properties and operating commercial buildings. It plans to raise funds to develop a shopping mall by offering digital tokens (“Token B”) to any person globally, including in Singapore. Token B will be structured to represent a share in Company B, and will be a digital representation of a token holder’s ownership in Company B. Company B also intends to provide financial advice in relation to its offer of Token B. Application of securities laws administered by MAS in relation to an offer of Token B.

B公司从事房地产和运营商业建筑的业务。 它计划通过发行Token B的方式,来向全球投资者(包括新加坡)募集资金,以开发一个购物中心。Token B被设定为代表B公司的股份,并将成为Token B持有者对该公司所有权的电子凭证。同时,B公司还打算就关于Token B的发行提供财务建议。Token B的发行适用于证券法,受MAS的监管。

在MAS的监管下,发行Token B适用于以下法规:

1. Token B will be a share and constitute securities under the SFA(Token B将成为股份并构成SFA下的证券);

2. The offer of Token B will need to comply with Prospectus Requirements, unless the offer is otherwise exempted under the SFA(Token B的发行将需要遵守招股说明书的要求,除非另有豁免);

3. Holders of a capital markets services licence that carry on business in dealing in tokens that are securities are required to comply with AML/CFT requirements under MAS Notice SFA04-N02(从事Token经营相关业务的资本市场服务牌照持有人必须遵守MAS通知SFA04-N02规定的AML / CFT要求);

4. Company B will not require a capital markets services licence for dealing in capital markets products that are securities under the SFA(在以下两种情况下,B公司在经营被SFA视为证券的资本市场产品时,可以不需要获得资本市场服务牌照):

if (a) it is not in the business of dealing in capital markets products that are securities (如果该公司没有从事经营被视为证券的资本市场产品的业务);

(b) it is in the business of dealing in capital markets products that are securities, but an applicable exemption applies. For example, if it is carrying on business in dealing in capital markets products that are securities for his own account through certain financial institutions regulated by MAS37, such as a holder of capital markets services licence to deal in capital markets products that are securities(如果该公司从事经营被视为证券的资本市场产品的业务,但适用于某个豁免条款。比如,该公司正在通过MAS37监管的某些金融机构,为了自身的利益,经营被视为证券的资本市场产品,例如让一个资本市场服务牌照的持有人来经营被视为证券的资本市场产品);

5. To provide financial advice in relation to its offer of Token B, Company B will need to be a licensed financial adviser, unless otherwise exempted(为了提供有关Token B提议的财务咨询,B公司将需要成为持牌照的财务顾问,除非另有豁免);

6. Licensed financial advisers are required to comply with AML/CFT requirements under MAS Notice FAA-N06(持牌照的财务顾问需要满足MAS通知FAA-N06下的 AML/CFT要求);

权威解读:

1、发行股票性质的代币需要满足的监管要求包括:获得资本市场服务牌照,两种豁免情况除外;满足MAS通知SFA04-N02规定下的AML / CFT要求;遵守公开招股书的相关规定,除非另有豁免。

2、当涉及到提供代币发行的财务建议时,公司需要获得财务顾问牌照,并满足MAS通知FAA-N06下的 AML/CFT要求,但在获得了资本市场服务牌照时,可以豁免该牌照的获取。

3、即使在豁免了财务顾问牌照的情况下,B公司也需要满足相应的报告要求,包括在Financial Advisers Regulations (Rg2)下的regulation 37(1)的要求,目的是为了让MAS了解到该公司正在FAA下,从事某项财务咨询业务;

案例6:Company F is planning to set up a digital payment token exchange platform that allows users to exchange digital payment tokens (such as Bitcoin) that do not constitute securities, derivatives contracts or units in CIS, to fiat currencies. In its initial years of operation, the platform will be configured such that trading of digital tokens constituting securities, derivatives contracts or units in CIS will not be allowed. This restriction may be lifted after a few years.

F公司正计划建立一个支付型代币交易平台,允许用户交易不构成证券、衍生品合约或信托单位的支付型代币法币,如比特币,到法币。在最初的几年,这个平台将被设定为不允许交易构成证券、衍生品合约或信托单位的代币,但这一限制可能会在几年后解除。

在MAS的监管下,发行Token F适用于以下法规:

1. On the basis that Company F’s digital payment token exchange will not allow trading of any products regulated under the SFA, the SFA will not apply(若F公司的支付型代币交易所不允许交易受SFA监管下的产品,那么SFA将不适用);

2. Company F should re-assess its position should it intend to trade in any digital tokens that constitute securities, derivatives contracts or units in CIS under the SFA(F公司应该再次评估其定位,是否打算开放受SFA监管的构成证券、衍生品合约或信托单位的代币的交易),

For instance, upon lifting the abovementioned restriction, Company F will likely be operating an organised market in relation to the trading of digital tokens that constitute securities, derivatives contracts or units in CIS. On this basis, Company F will then need to be approved by MAS as an approved exchange or recognised by MAS as a recognised market operator under the SFA, unless otherwise exempted(例如,一但解除了上述限制,F公司将很可能运营一个被组织的市场,当涉及到交易构成证券、衍生品合约或信托单位的代币。这样的话,F公司就需要被MAS批准,成为被认可的市场运营者(Recognised Market Operator,RMO),除非另有豁免);

3. Application of proposed PSB to Company F’s digital payment token exchange(应用已被提议的PSB在公司F的支付型代币交易平台中)。

Please note that while the activity of establising or operating a digital payment tokens exchange is presently not regulated by MAS, MAS intends to regulate such activity for AML/CFT purpose only under the PSB. Entities licensed under the PSB to perform such activities will be required to comply with AML/CFT requirements, including those relating to identification and verification of customer, ongoing monitoring, screening for ML/TF concerns, suspicious transaction reporting and record keeping. Company F must also abide by all Singapore laws, including theCDSA, the TSOFA and the UN Regulations, in the conduct of its business.

(值得注意的是,虽然成立或运营支付型代币交易平台目前不受MAS监管,但MAS打算仅在PSB下,以AML / CFT为目的监管此类活动。从事此类活动的在PSB下获得牌照的实体需要遵守相关的AML / CFT要求,包括客户的认证和验证、持续的监控、ML / TF问题筛查、可疑交易报告和记录保存。在业务运营时,F公司也必须遵守所有的新加坡法律,包括包括CDSA,TSOFA和联合国法规。)

权威解读:

1、比特币这样的支付型代币不构成SFA下的证券,因此支付型代币交易平台目前不受监管,但在PSB推出后,支付型代币交易平台需要获得PSB下的牌照并遵守相关的AML / CFT要求;

2、当涉及到提供构成证券、衍生品合约或信托单位的代币时,交易平台就需要经过MAS批准,获得受认证的资本市场运作者(Recognised Market Operator,“RMO”)牌照,除非另有豁免;

3、值得一提的是,这个案例在去年的版本中,MAS的表述为虚拟货币交易平台(Virtual Currency Exchange Platform),在更新版中变为支付型代币交易平台(Digital Payment Token Exchange Platform),这不仅表明了MAS已落实对代币分为证券型、应用型和支付型三类进行监管,且除了对应用型代币仍不监管外,将支付型代币明确纳入PSB监管框架。

以下是MAS所列出的11个案例中,所涉及到的公司和代币属性、注册地、业务地、融资范围以及相关监管法规的全面归纳总结:

“新加坡终极版合规指南与STO前景”

在全面解读了新版《指南》中所增设和强调的重点,以及对11个案例进行了专业透彻的分析后,我们为计划在新加坡进行STO、开设交易所的公司总结出了终极版本的合规指南:

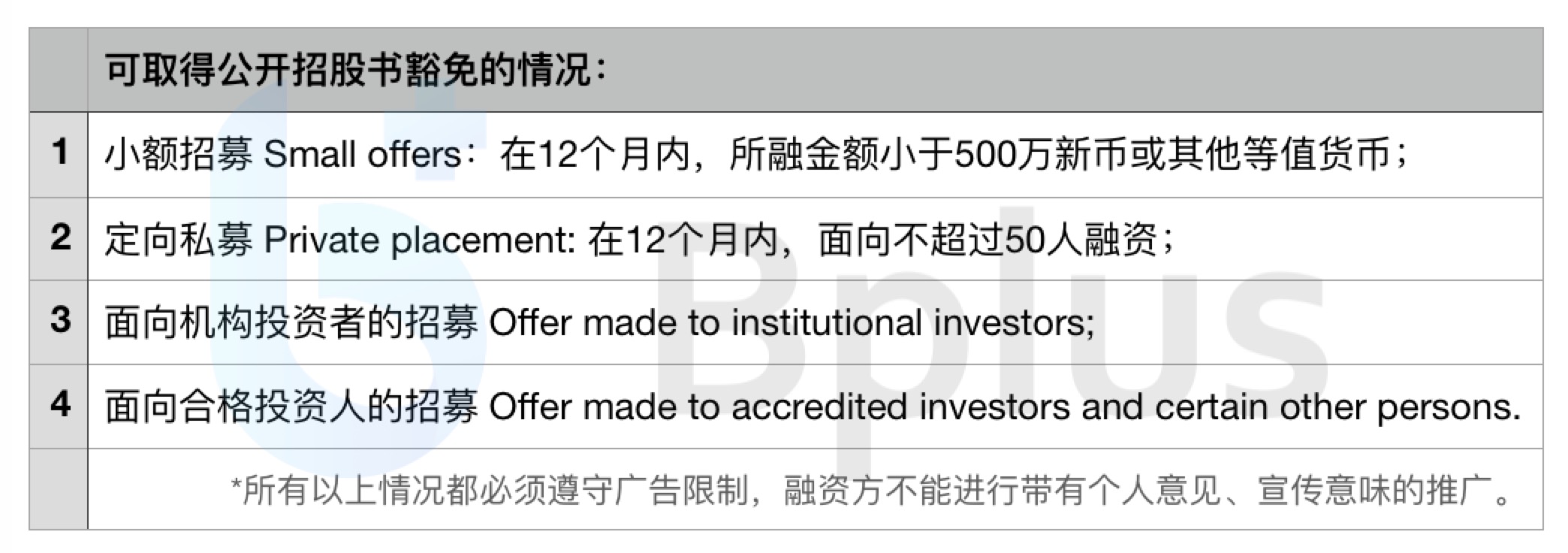

1、在涉及到发行证券性质的代币时,包括股票、债券、集合投资计划(“CIS”)单位基金、单位商业信托基金、基于证券的衍生品合约,需要获得资本市场服务牌照,并满足MAS通知SFA04-N02规定下的AML / CFT要求;此外,发行方还需要遵守公开招股书的相关规定,除非另有豁免,可豁免的情况请参考下图;

2、在涉及到提供代币相关的财务咨询服务时,需要在FAA下,获得财务顾问牌照,并满足MAS通知FAA-N06下的AML/CFT要求;

3、在涉及到交易证券性质的代币时,交易平台需要在MAS批准下,获得受认证的资本市场运作者(RMO)牌照后开展相关业务;

4、在涉及到支付型代币时,如比特币,相关机构均需要在PSB的监管下开展相关业务,支付型代币交易平台则需要在PSB生效后获得牌照,并满足PSB下的AML/CFT 要求;

5、在涉及到不构成以上所提及的代币类型和其他情况下, 在运营代币相关业务时,需要遵守所有的新加坡法规,包括CDSA,TSOFA和联合国法规。

由此可以看出,随着MAS更新版《指南》的公布,新加坡监管机构对代币的发行和交易都有了更加清晰的监管,并把所有的代币类型和交易所都纳入了监管框架。同时,对时下正热的STO,MAS也扩大了证券型代币的涵盖范围,给正计划开展相关业务的企业提供了可供参考的监管案例。

这意味着,在不断完善的监管制度下,新加坡未来的代币生态将继续茁壮成长。

- 免责声明

- 世链财经作为开放的信息发布平台,所有资讯仅代表作者个人观点,与世链财经无关。如文章、图片、音频或视频出现侵权、违规及其他不当言论,请提供相关材料,发送到:2785592653@qq.com。

- 风险提示:本站所提供的资讯不代表任何投资暗示。投资有风险,入市须谨慎。

- 世链粉丝群:提供最新热点新闻,空投糖果、红包等福利,微信:juu3644。